Blogs

In a previous article, Zenith covered Theme 1.1 of the A Level Economics syllabus, Scarcity as the Central Economic Problem, applicable to both H1 and H2 students. Do check out the article if you have any misconceptions on Scarcity before reading this one on Theme 2.1: Price Mechanisms and its Applications! As the leading Singapore JC tuition center, Zenith strongly advocates having a strong grasp of Scarcity as it underlies the entire A Level Economics syllabus. Understanding it well will therefore make all other themes, including Theme 2.1, much easier to comprehend. On that note, let’s take a look at what Theme 2.1: Price Mechanism and its Applications consists of by referring to Fig 1 below. In this article, we’ll be covering Themes 2.1.1. and 2.1.2 in an in-depth manner. Theme 2.1.3 will be covered in a second article, Part 2 of Theme 2.1: Price Mechanism and its Applications.

Fig 1. Overview of Theme 2.1: Price Mechanism and its Applications, as in the A Level Economics syllabus provided by SEAB

The first concept to figure out when approaching Theme 2.1 is that of the price mechanism. What is the price mechanism? The price mechanism is simply the decision-making tool through which consumers indicate to producers the amount of money they are willing to pay for a particular good or service and through which producers decide what good or service to produce and how much, how, and for whom they are going to produce it for.

More importantly, Theme 2.1 furthers the concept of Scarcity by considering the effects of economic actors having limited resources and unlimited wants on the market. First of all, we have to ask, what is a market? A market is the place where the interaction between buyers and sellers occurs. It is characterised by the concepts of demand and supply. What then is demand and supply? Demand refers to the quantities of a good or service that consumers are willing and able to buy at various prices during a period of time, ceteris paribus. Supply refers to the quantities of a good or service that producers are willing and able to sell at various prices during a period of time, ceteris paribus. Now, you might be wondering, what in the world is ceteris paribus? Why is the A Level Economics syllabus full of technical jargon? There’s no need to fret––you’ll get used to them over time as you invest time, effort, and resources into mastering the subject! Furthermore, many of these specialised terms actually have really simple meanings. Ceteris paribus, for instance, simply means “other things being equal” in Latin. Assuming ceteris paribus is necessary because we typically only want to study the relationship between any two variables (e.g. how taste and preferences affect price) at one time. The concept is similar to when you conduct a Science experiment; you only want to test the relationship between two specific variables at any one time, and you do this by ensuring all the other variables are constant (essentially what ceteris paribus means).

Now that we have gotten the definitions out of the way, let’s understand how the concepts of demand and supply each work before analysing how they affect each other.

Demand is affected by purchasing power, which is contingent upon desirability and affordability. When a consumer is willing to buy a particular good or service AND is able to pay for it, demand is created.

As seen in Fig 2, the highest point of the demand graph indicates the maximum price consumers are willing and able to pay for each quantity of Good A. When deciding whether they should purchase something, consumers try to perceive the satisfaction they will get from consuming the good or service. This is referred to as “utility”. The Law of Diminishing Marginal Utility (LDMU) states that as more and more units of a good or service are consumed, the additional (marginal) utility derived from consuming the good or service decreases, despite total utility increasing. As marginal utility decreases, the price that consumers are willing to pay for the good or service decreases. To put it simply, the more quantity someone has of a certain good, the less each unit of the good will make them satisfied, and thus, they become less willing to pay for it. The Law of Demand thus states that an inverse relationship exists between the price and the quantity demanded of a good, which means that as price increases, quantity demanded decreases.

At this point, it is apt for us to ask, what about non-price factors affecting demand? Indeed, there are 5 factors that will affect the demand of a good, which are not related to the price of the good itself:

1. Changes in Prices of Related Goods

Substitutes are goods that satisfy the same consumer desires. The decrease in the price of a particular good or service causes the demand for a substitute to decrease. For example, if the price of Starbucks coffee decreases, the demand for Coffee Bean coffee is likely to decrease.

Complements are goods that, when used together, satisfy the same consumer desires. The decrease in the price of a particular good or service causes the demand for the complement to increase. For example, as the price of cars decreases, the demand for petrol will increase as more people begin to purchase cars.

2. Changes in Consumers’ Tastes and Preferences

Think about yourself a year ago. Did you wear the same clothes as you do now? Or have your tastes in fashion changed? Maybe you used to go out in hoodies all the time, but you prefer t-shirts now. The same thing happens for all consumers! As our preferences change, they affect the demand for a particular good or service. What is in trend at a particular time can easily affect consumers’ tastes and preferences. For instance, as coconut slushies become increasingly popular, the demand for the drink increases. However, no one knows if coconut slushies will still be popular a year from now! Once the craze for the drink is over, the demand for it is likely to decrease significantly (read also: shorter queues for Mr Coconut!).

Advertising and promotions can also affect consumers’ tastes and preferences. Effective marketing efforts can result in the demand for a good or service increasing, which will generate increased revenue for the producers.

3. Changes in Consumer Demographics

As a population shrinks or grows, or has an increase in the number of elderly or adolescents, or experiences any other similar changes, the country’s demand for goods and services changes. The increase in a country’s population causes the potential demand for many goods and services to increase. For instance, as a population grows, there will be greater demand for housing, transport, and healthcare services. The shift in the demographics of a country’s population also affects demand. For instance, if there is an increase in the number of babies in a country, it is likely that the demand for baby diapers, baby clothing, and baby food will increase correspondingly. Other demographics such as that of gender might also affect the demand for particular goods and services in a country. For instance, a country with more women might see a greater demand for cosmetics in comparison to a country where there are significantly more men than women. At Zenith, our team of dedicated educators curates clear and comprehensible notes explaining the key demographics to consider when conducting analysis at the A Level Economics examinations, making our students’ learning process much easier.

4. Changes in Consumers’ Income

An increase in income usually results in an increase in demand for a good or service. This is as the good or service becomes more affordable for the consumer when they have more money.

Goods whose demand increases as income increases are normal goods. The demand for normal goods is positively related to changes in income, ceteris paribus. This means that if income falls, the demand for the good is likely to decrease and vice versa. Goods whose demand decreases as income increases are inferior goods. The demand for inferior goods is inversely related to changes in income, ceteris paribus. This means that if income falls, the demand for the good is likely to increase and vice versa. For instance, as income decreases, the demand for goods at a value-dollar shop is likely to increase, relative to the demand for goods at Cold Storage and FairPrice Finest, which are known to sell more “premium” and hence higher-priced goods.

5. Changes in Consumers’ Expectations

What and how much of a particular good or service a consumer decides to buy in the present can be affected by their expectations of future changes in prices and income. For instance, if consumers expect that the price of the ASUS laptop they are eyeing at the moment will fall in the coming months, they are less likely to purchase it now, causing a fall in the demand for the ASUS laptop.

These 5 non-price factors affect the demand for a particular good or service. Zenith’s specially curated JC Economics Tuition Programme explains in detail how these factors function in relation to each other, providing you with relevant examples that you can include in your A Level Economics essays (applicable to H2 students only). Get some tips on how to approach the A Level H2 Economics essays here.

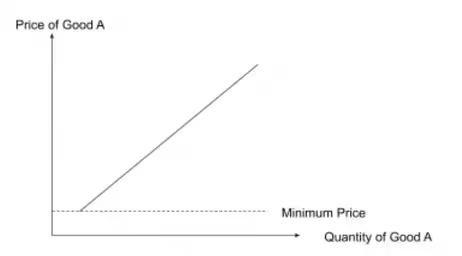

Supply is created when a producer is willing and able to supply a particular good or service at a particular price. In contrast to demand, supply is governed by the minimum (lowest) price, as to be seen in Fig 3. below.

While an inverse relationship exists between the price of a good or service and quantity demanded, a direct relationship exists between the price of a good or service and the quantity supplied, ceteris paribus. Quantity supplied increases as the price of a good or service increases as producers are driven by the profit motive, which means that they are more likely to want to produce goods or services with higher prices which will result in higher revenue and hence, higher profit.

Similar to demand, supply can also be affected by non-price determinants. There are 5 non-price factors that will affect supply:

1. Changes in Price of Related Goods

Competitive supply occurs when two particular goods or services use the same factors of production. When the price of Good A rises, the supply for Good B will decrease. For instance, land is required for the production of both rice and vegetables. If a piece of land is used for the production of the former, then it cannot be used for the latter. This means that if the price of rice increases, the supply of wheat will decrease. Such a situation occurs because producers, driven by the profit motive, will want to produce more rice when its price increases. With the same amount of land available, producers will have to plant lesser wheat if they decide to plant more rice. As such, the supply of wheat will decrease.

Joint supply occurs when two particular goods or services are produced together using similar factors of production. When the price of Good A rises, the supply for Good B will increase. For instance, timber and paper are jointly produced. When the price of timber increases, producers, driven by the profit motive, will increase the quantity supplied of timber. The supply of paper increases in the process as there is an increase in wood pulp, the factor of production required for making paper.

2. Changes in Cost of Production

Costs of production are affected by the price of factors of production, the state of technology, and government intervention in the form of taxes and subsidies, both direct and indirect. As the costs of production increase, producers have to spend a larger amount of money on the production of every unit of a particular good or service. This means that with the same amount of money available, they will produce lesser units of the good, causing supply to decrease. The reverse is also true, which means that as costs of production decrease, supply will increase.

3. Changes in Number of Producers of a Good

Market supply is determined by the total units of a good or service produced by all producers in the market. As the number of producers in the market decreases, market supply decreases and vice versa. For instance, the supply of burgers in Singapore has increased as Five Guys and Shake Shack entered the market, compared to when there was only McDonalds, Burger King, and KFC previously. Hence, we can observe how the market supply of burgers has increased with new entrants to the market.

4. Supply Shocks

Supply shocks occur when unpredictable events which are not necessarily within human control occur. For instance, a drought or flood will cause poor harvests for affected farmers, which reduces the supply of natural produce for consumers. While this might sound strange, supply shocks can also positively affect supply. For instance, a bumper harvest for various unexpected reasons will increase the supply of natural produce.

5. Changes in Producers’ Price Expectations

Producers, like consumers, have expectations of how the market will change in the future. If they expect that demand for specific goods will increase for various reasons, resulting in an increase in price, producers might temporarily hold back the goods, creating a drop in the current supply. They will increase the supply of the goods when demand and hence price increases, which will generate higher revenue for themselves.

These 5 non-price factors affect the supply for a particular good or service.

Interactions between Supply and Demand (Market Equilibrium)

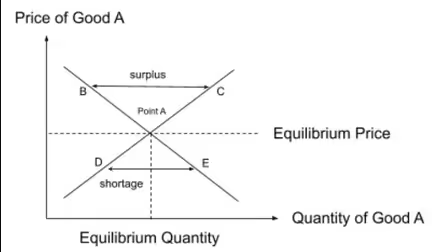

In reality, the forces of demand and supply do not work in a straightforward way. They are constantly affected by multiple factors at once, as we have just covered. This means that the market is rarely at its equilibrium point (Fig 4). Nonetheless, at the A Level Economics examinations, it is important that you understand how a competitive market without government intervention functions. In these markets, market equilibrium price and quantity refer to the price and quantity of a particular good or service being exchanged where the quantity demanded is exactly equal to the quantity supplied, ceteris paribus.

As seen in Fig 4, the market equilibrium is at the point of intersection (Point A) between the demand curve and the supply curve. At any other price, there is a mismatch between supply and demand. If the Price of Good A were to decrease further, quantity demanded will exceed quantity supplied, creating a shortage in the number of units of the good. This is graphically represented in the space between Point B on the demand curve and Point C on the supply curve. If the Price of Good A were to increase further, quantity supplied will exceed quantity demanded, creating a surplus in the number of units of the good. Similar to when there is a shortage in the number of units of a good being produced, the surplus of the number of units of a good being produced is graphically represented in the space between Point D on the supply curve and Point E on the demand curve.

With that, we have come to the end of Theme 2.1.1 and Theme 2.1.2 of Price Mechanism and its Applications. As a quick recap, Zenith has covered the following concepts in this article:

The remaining portions of Theme 2.1 will be covered in a subsequent article. In the meantime, it is extremely important that you familiarise yourselves with the concept of demand and supply, as a majority of the remaining themes under Microeconomics require a strong understanding of its key concepts.

Find out more about Zenith’s top tuition programme for A Level Economics here, and sign up for a free trial lesson by contacting us here!

Explore resources and strategies for learners at every stage

.avif)